The federal Bureau of Labor Statistics reported today that year-on-year “inflation” through June was 9.1 percent, meaning the basket of goods constituting the “consumer price index” (CPI) that cost $100 a year ago cost $109.10 last month.

That’s bad news, for several reasons.

First, of course, it’s bad news because it means life gets tougher for everybody whose income isn’t enhanced by precisely those things that drive such “inflation”—meaning the vast majority of people.

Second, it’s bad news because it’s 0.5 percent higher than the year-on-year “inflation” through the previous month, which means “inflation” didn’t peak at 8.6 percent in May, as many predicted it would, but continued to climb. What’s worse is that even most economists missed this one. The Dow Jones, for instance, had predicted that June’s year-on-year rate would be 8.8 percent, up 0.2 percent from May. That it was up 0.5 percent instead shows how very bad the prediction was off: the actual increase was 2.5 times the prediction. That suggests the experts’ grasp of the underlying factors is dismal.

Third, it’s bad news because what lifted the year-on-year rate from May’s 8.6 to June’s 9.1 percent was June’s rather astonishing single-month “inflation” rate of 1.4 percent. Annualize that and you get year-on-year “inflation” of 16.8 percent—meaning the CPI $100 basket of goods at the start of such a year would cost $116.80 at its end. That’s not hyperinflation, but it’s staggering. Clearly, we’re in deep trouble if this “inflation” rate isn’t reined in.

Oh, and the real news is even worse. The CPI is, in fact, a poor representation of the everyday prices Americans pay for everyday purchases, because the “basket of goods” it represents hasn’t been revised enough over the decades to reflect our changing society and its economy. The American Institute for Economic Research maintains an Everyday Price Index that is more realistic. By that, June’s single-month “inflation” rate was not 1.4 but 2.4 percent. Annualized, that’s 28.8 percent.

You might wonder why I’ve been putting scare quotes around “inflation” every time I’ve used it. It’s because real inflation isn’t rising prices. Those are the consequence of real inflation. Real inflation is an increase in money supply. If that increase is more rapid than the increase in the supply of goods and services people can buy, prices of goods and services rise; if it’s slower, prices fall; if it’s identical, prices remain unchanged. Assuming the supply of goods and services remains unchanged, a 10 percent rise in money supply will cause a 10 percent rise in prices, while a 10 percent decline in money supply will cause a 10 percent decline in prices.

Our government and the Federal Reserve Bank keep calling rising prices “inflation” to blind us to the role changes in money supply play in those rising prices. Classical economics defined inflation as an increase in money supply. Call it an increase in prices instead, and people don’t blame it, as they should, at least in part and often in whole, on monetary policy. People will blame producers and distributors for “excess profits” driven by “greed” instead of government and the Fed for stealing through what is morally no different from counterfeiting.

Our government tells us that our “inflation” rate (the rise in CPI) is primarily because of reduced production and distribution (supply chain) due to the COVID-19 pandemic (more properly, due to government responses to the pandemic—those, not the disease itself, caused most of the supply chain problems). That’s only partly true. Had production and distribution declined while money supply remained the same, prices would have risen, but not as much.

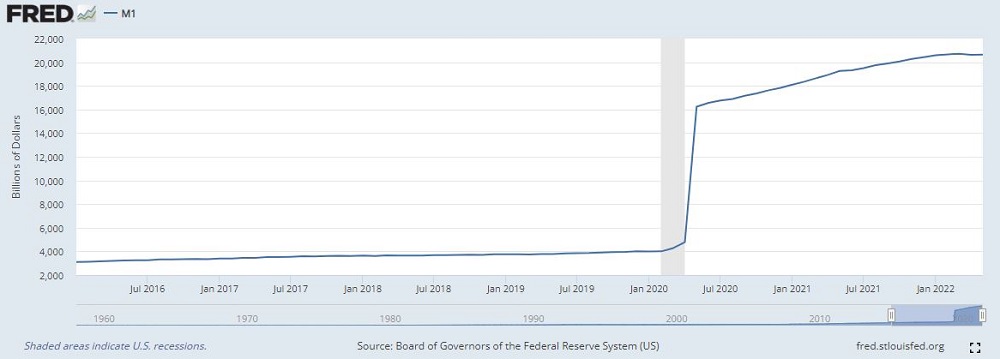

So, did an increase in money supply (real inflation) contribute to the rising CPI (what is falsely called “inflation”)? A quick look at this graph, generated on the website of the St. Louis Fed, should answer that question.

That depicts what happened to “M1” money supply from January 1, 2016, through May 1, 2022. “M1” comprises demand deposits, savings deposits, and other liquid (quickly and easily traded) deposits; it doesn’t count bonds and similar illiquid financial assets.

In January 2016, M1 was $3.097 trillion. In January 2020, it was $3.994 trillion—up by $897 billion, or 29 percent in four years. Absent a major expansion of production of goods and services, that would have driven about a 7 percent annual increase in CPI, but that major expansion did take place.

By May 2020, however, M1 was $16.233 trillion, up by $12.239 trillion, or 306 percent in four months. Think the mad spree of “making” “money” out of thin air stopped then? Think again M1 peaked at $20.71 trillion in March of this year, up $4.48 trillion or 48 percent in 22 months. M1 in May of this year was $20.633 trillion, up $16.639 trillion, or 417 percent, since January 2020. The increase in M1 in the 29 months from January 2020 through May 2022 was 5.4 times the total M1 in January 2016.

Clearly there aren’t 5.4 times as many houses, cars, loaves of bread, gallons of gas, pairs of socks, surgeries, massages, legal representations, and whatever other goods and services you can imagine now as there were twelve years ago. It follows necessarily that the dramatic real inflation must have contributed to today’s dramatic so-called “inflation.”

Elected officials have an ingrained incentive to perpetuate real inflation—increased money supply. Why? Because it’s the sneakiest, least understood means of taxation and thus the easiest way to pay for the programs they use to buy votes but aren’t willing to pay for by clearly visible taxation.

The central banks and the large banks that first use newly created “money” also have an ingrained incentive to perpetuate real inflation. They get to use the newly minted (or digitized) “money” at its pre-“inflation” value, before the larger market devalues it relative to goods and services. Until enough Americans grasp this to demand that elected officials abandon this policy, we will see bouts of “inflation” like the present come again and again, always hurting the little guy while helping the elites in and out of government. Remember that the next time you head for the ballot box—and make your elected representatives remember it, too.

Thanks you for your sage analysis of the situation!